Despite rising prices and food costs that stretch consumer dollars, inflation has not had much effect on retail meat demand, said Brian Earnest, Lead Animal Protein Analyst at CoBank. Compared to last year, inflationary conditions are improving, but supply constraints are continuing to place upward pressure on animal proteins and affect prices this spring and summer. Consumer behavior shifts are expected to continue this year as interest rates rise and consumer savings erode.

All things considered, Earnest is optimistic about demand at the meat case. According to a study from the University of Michigan, U.S. consumer sentiment is improving after years of significant declines.

Animal Protein Demand

In 2022, meat sales reached a record $87 billion, a 6% increase over the previous year. This happened despite a 3% volume decline, about 600 million units, year-over-year. Data included fresh beef, chicken, pork, and turkey.

“I think overall, it is clear consumers are willing to spend more at the meat counter,” Earnest said. “Beef demand has been exceptional.”

For context, retail beef consumption declined from 2009-2015 as prices climbed an average 7% per year, according to USDA data compiled by CoBank. In response, retail beef prices slowed from 2015-2017, rising 2% on average.

Since the pandemic, beef disappearance has not slowed, despite retail prices increasing 9% or more each year.

Animal Protein Production

Protein production is expected to moderate after years of growth. Beef is going through significant supply constraints after intense drought forced ranchers to sell off their cattle herds. Cattle slaughter increased more than 11% in 2022 compared to the prior year. The national herd count was down 3% as of Jan. 1.

Pork is seeing a moderate rebound. Despite hog inventories being down, growth in the breeding herd size suggests potential growth in the back half of 2023. Rising feed costs are hampering chicken growth this year after stronger than expected production in 2022.

Summer Grilling

For a bacon cheeseburger, meat cuts and formulations are looking favorable ahead of the summer months. Beef grind formulations are above historical norms, but lower than when they peaked in 2020, especially for 50s. Recent data show they are going for less than $125 per hundredweight. Meanwhile, the pork belly primal is down 20% compared to a recent 5-year average. It is valued at roughly $100 per hundredweight.

For middle meats, such as ribeye and brisket, prices are above the 5-year average from 2017-2021, but lower than what they were in the fourth quarter. Ribeyes have declined in value since January 2023, but are starting to rebound. They are valued at roughly $450 per hundredweight. Briskets steadily declined last year, but they remain 17% above the 5-year average. Recent data show briskets valued less than $200 per hundredweight.

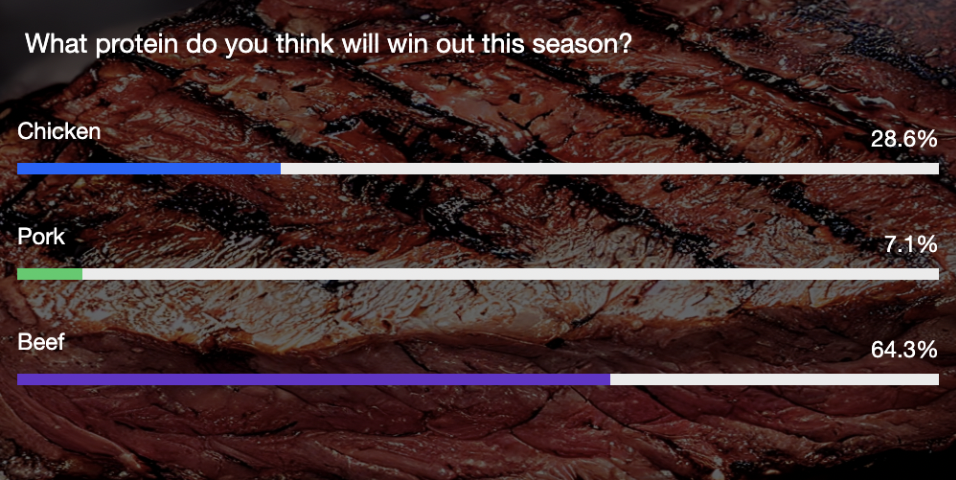

Audience Poll

What animal protein will be most popular this grilling season? Most attendees selected beef as their favorite, followed by chicken and pork. Michael Nepveux, Lead Protein Analyst at Stable, and Earnest agreed with the audience consensus.

Overall

Macro conditions are continuing to pressure consumer spending, but so far, meat demand has been stronger and more resilient than expected. Earnest said the grilling season will be full of challenges as producers continue to adjust to inflation.

Animal Protein Demand

In 2022, meat sales reached a record $87 billion, a 6% increase over the previous year. This happened despite a 3% volume decline, about 600 million units, year-over-year. Data included fresh beef, chicken, pork, and turkey.

“I think overall, it is clear consumers are willing to spend more at the meat counter,” Earnest said. “Beef demand has been exceptional.”

For context, retail beef consumption declined from 2009-2015 as prices climbed an average 7% per year, according to USDA data compiled by CoBank. In response, retail beef prices slowed from 2015-2017, rising 2% on average.

Since the pandemic, beef disappearance has not slowed, despite retail prices increasing 9% or more each year.

Animal Protein Production

Protein production is expected to moderate after years of growth. Beef is going through significant supply constraints after intense drought forced ranchers to sell off their cattle herds. Cattle slaughter increased more than 11% in 2022 compared to the prior year. The national herd count was down 3% as of Jan. 1.

Pork is seeing a moderate rebound. Despite hog inventories being down, growth in the breeding herd size suggests potential growth in the back half of 2023. Rising feed costs are hampering chicken growth this year after stronger than expected production in 2022.

Summer Grilling

For a bacon cheeseburger, meat cuts and formulations are looking favorable ahead of the summer months. Beef grind formulations are above historical norms, but lower than when they peaked in 2020, especially for 50s. Recent data show they are going for less than $125 per hundredweight. Meanwhile, the pork belly primal is down 20% compared to a recent 5-year average. It is valued at roughly $100 per hundredweight.

For middle meats, such as ribeye and brisket, prices are above the 5-year average from 2017-2021, but lower than what they were in the fourth quarter. Ribeyes have declined in value since January 2023, but are starting to rebound. They are valued at roughly $450 per hundredweight. Briskets steadily declined last year, but they remain 17% above the 5-year average. Recent data show briskets valued less than $200 per hundredweight.

Audience Poll

What animal protein will be most popular this grilling season? Most attendees selected beef as their favorite, followed by chicken and pork. Michael Nepveux, Lead Protein Analyst at Stable, and Earnest agreed with the audience consensus.

Overall

Macro conditions are continuing to pressure consumer spending, but so far, meat demand has been stronger and more resilient than expected. Earnest said the grilling season will be full of challenges as producers continue to adjust to inflation.

Brazilian “Mad Cow” Case

A case of bovine spongiform encephalitis, also known as mad cow disease, was confirmed in the northern state of Para last week. This led to China halting Brazil’s beef exports from entering the country.

Reuters recently reported the infected animal was on a property with 160 head of cattle and that samples were sent to the World Organization for Animal Health lab in Alberta, Canada to confirm whether it was a classic or “atypical” form of the disease.

During the webinar, Nepveux said Brazil’s agriculture and livestock ministry indicated that it was not a “classical case” of the disease and that China’s temporary action is not necessarily a punishment toward Brazil, but based on a previous agreement between the two countries. In terms of global trade, he said “we’re likely not going to see this as a big disruption.”

The “R” Word

The recession is on the minds of economists, analysts, and other market-followers, but most hesitate to say it outright. “That’s the issue the Fed is dealing with right now,” Earnest said. “They want to ‘thread the needle’ with higher interest rates to cool things down…if we are headed toward one, it’s going to look much different than any previous recession period.”

Historically, during recessions, consumers shifted away from buying services to buying more goods. “This doesn’t look like that,” Earnest said.